Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Seller Series – Part 1: You Never Get a Second Chance to Make a First Impression

So, you’re thinking about selling your home in 2026. The best time to start preparing is right now. Properly preparing your property for sale takes time, and that time passes quickly. The phases of preparation range from decluttering your home and removing many of the clothes you don’t need from your closets, to tackling those repair issues you’ve been ignoring for years. The goal is to make your house the most attractive house on the market in your price range. This 5-part Seller Series – Preparing Your Home For Sale in 2026 – will give you a view of the multi-faceted process of selling your home.

Time is your friend

You cannot control which neighborhood houses will be on the market, or how many buyers will be actively shopping your neighborhood, when your time to list comes around. The trick is to make your house look more attractive than anything else on the market at go time. Starting early gives you plenty of time to identify the projects and find the professionals to help complete those projects. The sooner you start the process, the less stress you create as you get closer to your listing date.

Step One – Let’s Talk Preparation

As your real estate advisor, one of my jobs is to help you prepare your house for sale by identifying the projects that should be done and those that can be done if you choose, all within your budget.

“You never get a second chance to make a first impression.”

That old adage is the basis of my advice to create a great first impression for buyers when they see your home online and in person. That impression starts at the street, works its way up to the front door, and then peaks when they open the front door. Landscaping and tree trimming, pressure washing, painting, repairing front steps and porches, cleaning and staging the inside of the house.

Then we get to look under the hood. I have experienced many inspections over the years as a representative of both buyers and sellers. I know the issues that home inspectors are likely to identify, and which issues are likely to be the subject of negotiations prior to closing a sale.

The items that come up frequently are furnaces, air conditioners, water heaters and roofs. The issues that are often the most surprising are the ones you can’t see. These include: the condition of the sewer line; mold in the attic or crawl space; and crawl space issues like water intrusion, rodents, poor vapor barrier and/or insulation, and radon. Identifying and correcting these types of issues before you list your home for sale will go a long way toward avoiding a difficult post-inspection negotiation.

Let the home inspectors find little items to address, but don’t let them surprise you with major repairs or discoveries that may scare off buyers and prolong the time your house takes to sell.

As you contemplate selling your home, let’s talk about preparing your home for sale and the time it will take to do it right.

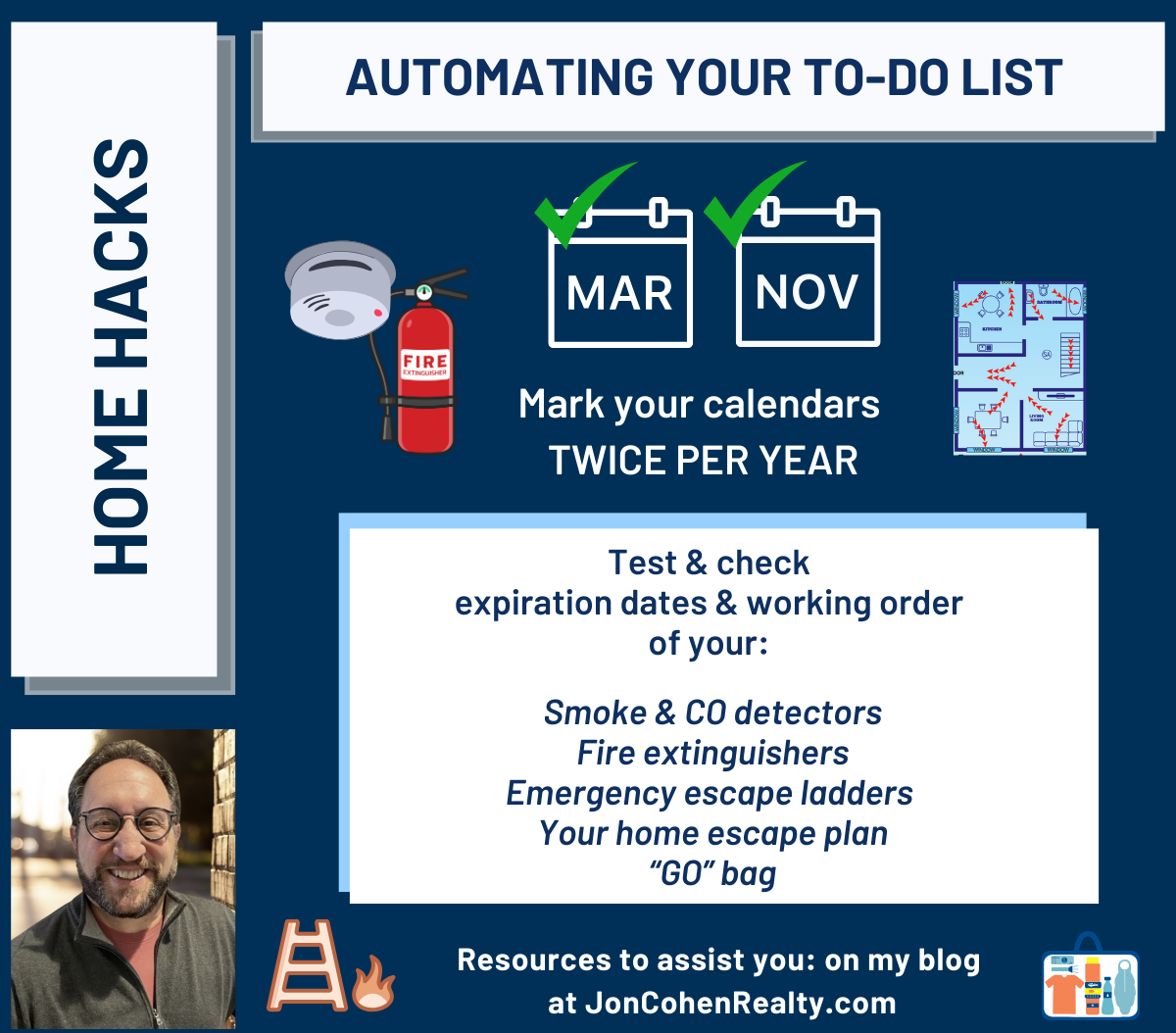

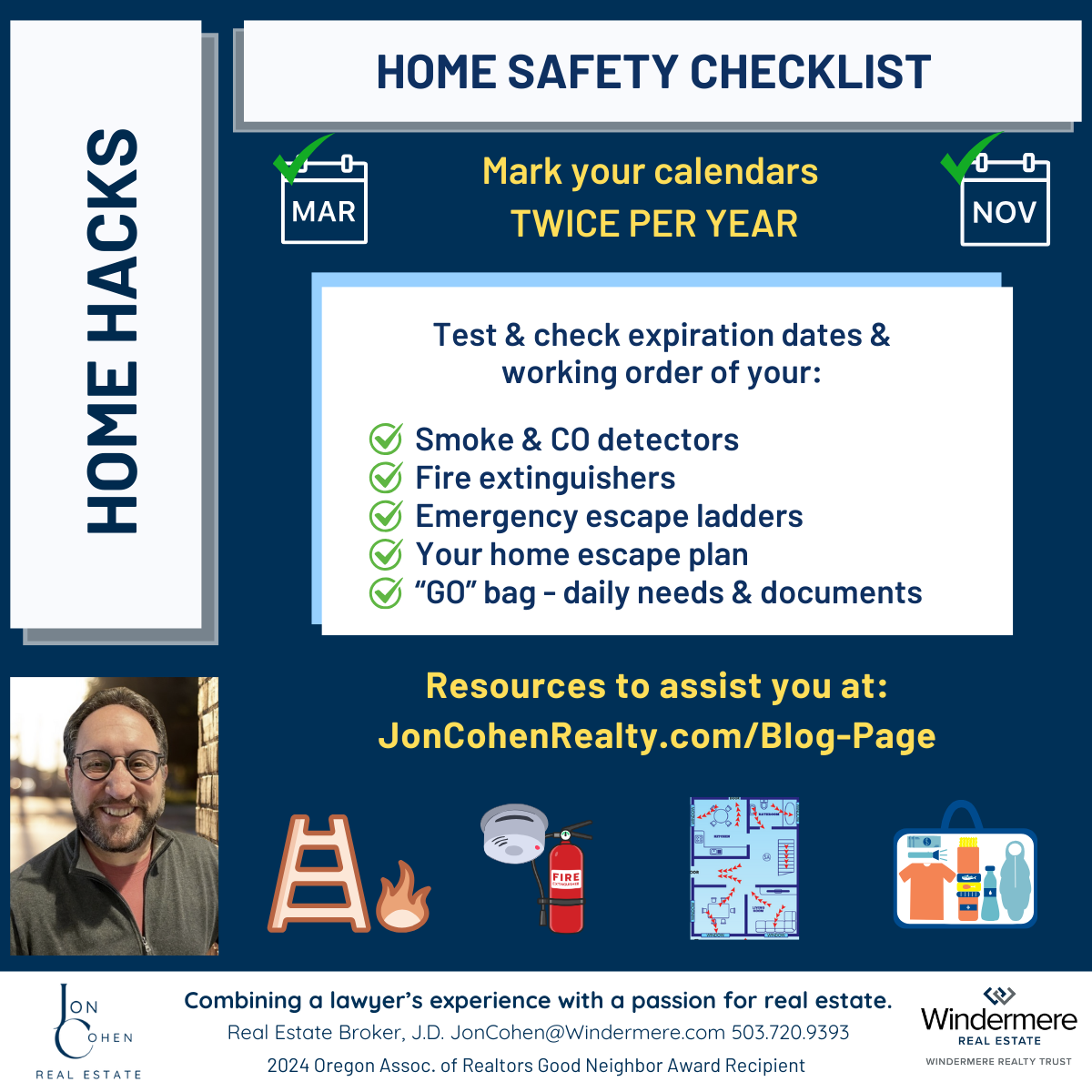

Your Home Safety Checklist

Your Ultimate Home Safety Checklist

Ensuring the safety and well-being of your family is a top priority, and taking proactive steps to prepare for emergencies can make all the difference in protecting your loved ones and your home. Here’s a home safety checklist to help ensure you’re well-prepared for any situation.

1. Check Smoke and Carbon Monoxide Detectors

Smoke and carbon monoxide detectors are your first line of defense against fire and gas emergencies.

- Test alarms regularly, at least once a month.

- Replace batteries annually or when the low-battery warning chirps.

- Ensure there’s a detector on every level of your home, including the basement.

- Replace detectors every ten years or as recommended by the manufacturer.

2. Inspect Fire Extinguishers

Fire extinguishers can help control small fires before they become big emergencies.

- Make sure extinguishers are easily accessible and not blocked by furniture or other items.

- Check the pressure gauge to ensure the extinguisher is fully charged.

- Ensure the extinguisher is not more than ten years old.

- Confirm you have the correct type of extinguisher for different areas (e.g., kitchen, garage).

3. Create or Practice Your Home Escape Plan

Having a well-practiced escape plan can save precious seconds during an emergency.

- Draw a floor plan of your home, marking all exits and escape routes.

- Designate a safe meeting place outside your home where everyone will gather.

- Ensure all family members know how to exit safely from each room, even in the dark or smoke.

- Practice your escape plan twice a year, including the placement and use of emergency escape ladders on upper floors.

4. Prepare Your “Go Bag”

A “Go Bag” ensures you have essential supplies ready to go at a moment’s notice.

- Pack a three-day supply of non-perishable food and water (one gallon per person per day).

- Include medications, personal hygiene items, and basic first-aid supplies.

- Pack important documents such as identification (ID cards, passports), insurance policies, and financial records.

- Include items like flashlights, batteries, a multi-tool, blankets, and a whistle.

5. Necessary Documents for Emergencies

Keep important documents in a safe, easily accessible location, or have electronic copies available.

- Personal identification: driver’s licenses, passports, Social Security cards.

- Property records: deeds, titles, rental agreements, mortgage documents.

- Financial records: bank account information, credit card statements, tax returns.

- Medical information: health insurance cards, medical records, prescriptions.

- Legal documents: wills, powers of attorney, birth and marriage certificates.

By taking these proactive steps, you can ensure your home is prepared for emergencies and your loved ones are safe. Remember, regular maintenance and practice are key to effective home safety. Stay vigilant and keep this checklist handy to make sure you’re always ready for the unexpected. Stay safe! 🏡🔒

Your Phone Can Save Your Life

After a recent life-threatening medical event in our family, I want to share this important information to help you be better prepared. If you, your family, or friends are unable to communicate with emergency personnel—whether unconscious or otherwise incapacitated—it can be extremely difficult for responders to understand your medical conditions, allergies, medications, and emergency contacts. This can delay critical care and hinder their ability to reach the right people who can speak on your behalf. However, if this vital information is stored and updated on your phone, first responders can access it, even if your phone is locked, allowing them to provide timely treatment and potentially save your life.

Here are instructions to add this crucial information to your iPhone or Android phone:

For an iPhone:

For an Android phone:

TIP: Set a recurring date on your calendar to review and update your Medical ID entries every quarter, as any of this information may change (especially medications), and it is critically important that medical personnel are aware of potential drug interactions.

We’re All Waiting With Anticipation

![]()

Today was a big day for mortgage interest rates. Providing a positive vibe for the housing market, the average interest rate for 30-year mortgages dropped to 6.34%, the lowest rate since April 2023. The lower rates will help homebuyers concerned about affordability which in turn provides sellers with a bit more comfort about giving up their very low interest rate mortgages when they purchase their next home. With each 1% drop in interest rates, buyers gain approximately 10% more buying power.

Sellers have struggled with giving up their low interest loans and many decided to stay in their homes rather than sell. This contributed to the low inventory of homes available to buyers. At the same time, buyers have struggled with affordability issues as high interest rates combined with higher prices due to the limited supply of homes. There is hope that as interest rates come down, we will see more "elective" sellers put their homes on the market, and more buyers will be able to afford to purchase.

Will interest rates continue their downward trend? We'll have to wait and see. It's possible that the lending community is building in lower rates before the Federal Reserve takes action in September. Or the markets could be reacting to other economic factors and could lower rates if and when the Fed lowers its rate. Some economists have predicted increased real estate activity if interest rates come down to 6%, which is not too far away. The whole real estate industry will be waiting with anticipation.

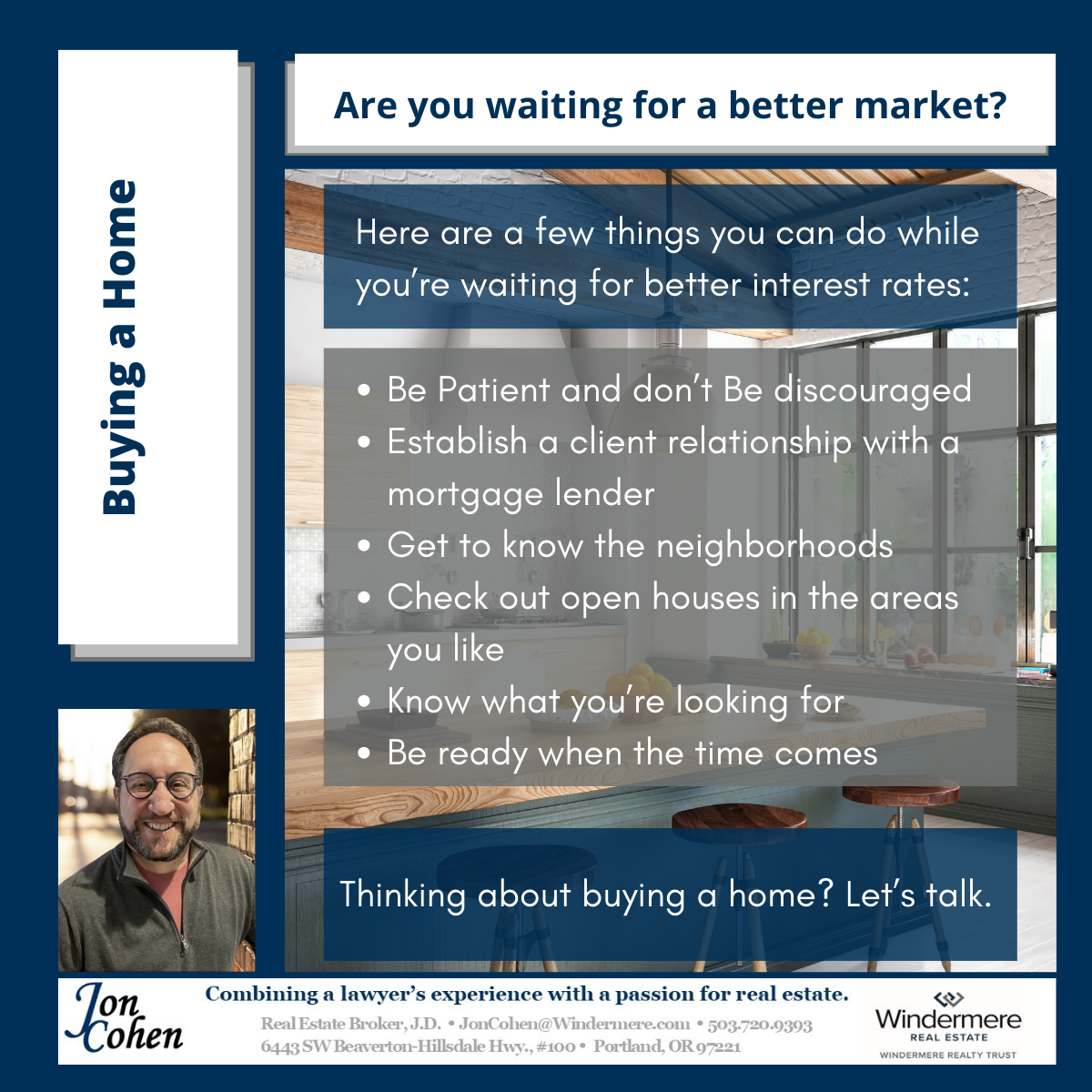

Homebuyers – Don’t Be Twiddling Your Thumbs While Waiting For Better Interest Rates

Many Homebuyers today are feeling caught between higher interest rates and rising home prices. They want to buy now because home prices are increasing, while at the same time, they want to wait until interest rates come down a bit – hopefully later this year. If you choose to wait for better interest rates, here are a few things you can do

If you want to buy a house and are waiting for better interest rates, here are a few things you can do while you wait to be sure you are ready to go when the time comes.

Have patience and don’t be discouraged!

The right house will be out there and will be available for you to make your offer when the right time comes.

Get to know a mortgage lender and establish yourself as a client.

Before you go looking for a home, you need to know how much you can afford. Have the lender give you full approval subject to finding the right home. I know some great lenders and would be happy to introduce you.

Get to know the neighborhoods

If you don’t know exactly where you want to live, check out different parts of the city. Walk around the neighborhoods and check out some local restaurants, pubs, and coffee houses. Meet some people and let them know you’re looking to buy and want to learn something about the neighborhood. The neighbors often hear about houses coming on the market before the real estate brokers and the general public, so keep your ear to the ground.

Check out open houses in the areas you like.

This will give you a sense of the types of homes in the area, the condition of homes, and the difference between a good remodel and a home that needs some work.

Know what you are looking for.

Use this time to get a good feel for what you want and need in your new home. Talk with me and let me know what you like and don’t like. I can keep an eye on the neighborhoods you like and be ready to help you as soon as you know you’re ready to jump in.

Be ready when the time comes

Great houses are still getting multiple offers. You will be ahead of the game if you have everything ready to go when that perfect house comes to market.

Buying a home is an exciting process. When you are ready, I can help you through the process with the patience and determination to help you find your new home.

Let’s talk!

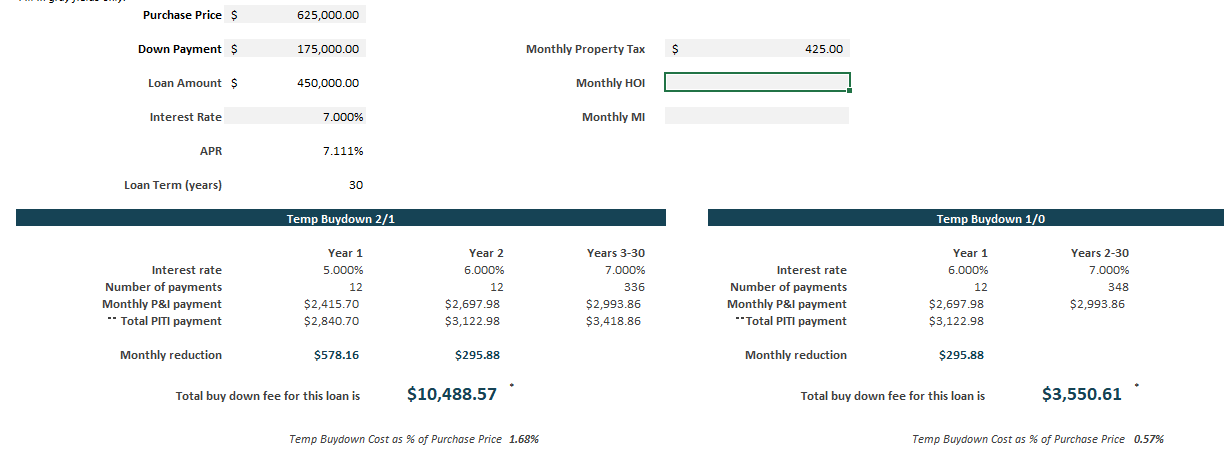

Interest Rate Buydowns Help Buyers and Sellers

When interest rates were at historic lows, a typical fixed-rate mortgage loan was all most people needed. Now, with rates appreciably higher, buyers’ monthly mortgage rates are much higher. As the real estate market adjusts to changing interest rates, buyers and sellers are looking to make homes more affordable, and lenders are helping with interest rate buydown loans.

For a home that has been on the market for a while, the seller could lower the price $25,000, OR offer a $10,500 credit to buy down the mortgage interest rate, saving $14,500 and creating a more affordable monthly payment for the buyer. The illustration below is an example of how an interest rate buydown can save the buyer money each month.

In this example – a “2/1 Buydown” – the buyer will get a 30-year fixed rate loan with an interest rate that’s discounted 2% during the first year and 1% the second year. The buyer will ease their way into a new home with lower payments that simply step up at the end of the first and second year, and then remain fixed for the remainder of the loan.

This is just one way today’s buyers can make buying the home they really want a reality. At the same time, sellers can offer an incentive to buyers without a dramatic price reduction. If you have any questions or would like to learn more, let’s talk.

So Inventory is Still Low

I often get questions about the real estate market and hear how so many news stories report on the extremely low inventory of homes to buy. Don’t let the news stories scare you. The reality is that there are properties to buy; they’re just not on the market very long. We have pending transactions. We have closed sales. And we have satisfied buyers and sellers. We also have some frustrated buyers and sellers for different reasons.

My advice for sellers is to be prepared. Here are a few ways for sellers to prepare their property and themselves for the market:

- Make sure your home is “Ready for Prime Time.” Your property must make a great first impression, and your first impression will be online. Make sure that your house shines, from paint to flooring to landscaping. The photos you use online must show your home at its best.

- Be aware of maintenance issues in your house. If you can make necessary repairs, do so before hitting the market. If not, be prepared to negotiate repair issues with buyers.

- Be realistic about pricing your property. Buyers have been in the market longer and are savvy about pricing. Be sure you know what’s happening with pricing in your neighborhood – real estate is local – even hyper-local.

If you are thinking about putting your house on the market, the houses selling are priced appropriately and well-counseled sellers are not insisting on pricing their homes too high. The best thing for sellers to do is price their homes within the range of comparable sales in the area, and then let the buyers determine the actual market value. Some buyers will offer more than your list price. However, if you assume that buyers will pay more than the comparable prices in your area, you may price it too high and not receive any offers. The buyers will tell you the best price for your home. If you price your home too high, or if your home is not “Ready for Prime Time” when it is first exposed to the market, you will find that your home will sit on the market longer than average. And sometimes a house may have some unique features that only particular buyers may want, so you’ll need to be patient until those buyers come along.

My advice for Buyers is to be prepared and be patient. Here are a few ways that you can prepare yourself to be a home buyer:

- Before you begin your home search, meet with a lender and ask for a lender pre-approval letter. This will allow you to determine how much you can comfortably spend for your new home, and give sellers some assurance that you will qualify for the loan and successfully close the sale.

- Make sure your down payment funds are available on short notice. If you do not have the cash readily available, be sure you know which assets you will liquidate (stocks, bonds, etc.) and how long it will take for you to receive the funds.

- Make your offer with a good earnest money deposit. Earnest money between one and two percent of the purchase price (or more if you are comfortable) will signal to the seller that you are serious about the purchase and willing to put your own money at risk until the closing.

These three items will show that you are ready to buy right now and ready to make the best offer possible. With continued low inventory, there are many qualified buyers waiting for the right house to come on the market, so we are still seeing multiple buyers making offers for the same property. Depending on the situation, buyers can offer certain enticements to sellers (like shortening the inspection period or even waiving the right to inspections) in hopes they will accept an offer. There are several additional “seller enticements” that can be added to an offer, so long as you are comfortable with the terms.

Overall, my advice to both buyers and sellers is to be patient. For buyers, the right house at the right price with the right seller will cross your path. For sellers, your patience is important at the front end – getting your house ready for sale, making the best first impression, and setting the right price. And your real estate professionals also need to be patient at each step. If you have any questions about this information, let’s talk.

Market Statistics For February 2023

Here are the Market Statistics for February 2023. The average and median sale prices decreased by 5.3% and 3.7% respectively. While buyers and sellers will look at these numbers differently, I’m curious to see if this will be a continuing trend or simply the result of our unusually slow winter sales cycle. I believe it will be the latter, with prices rising moderately over the next few months.

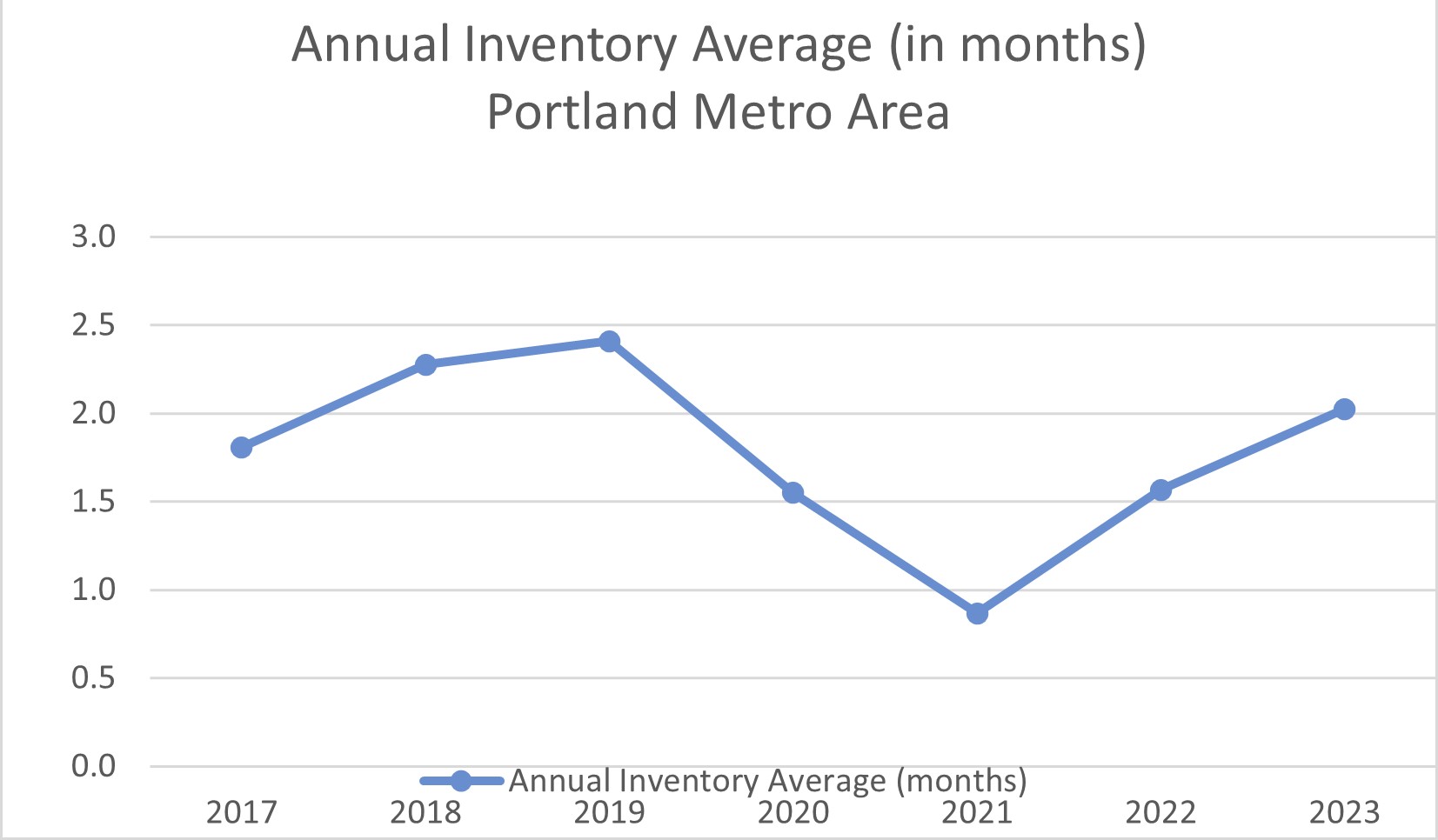

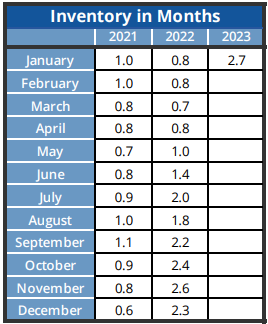

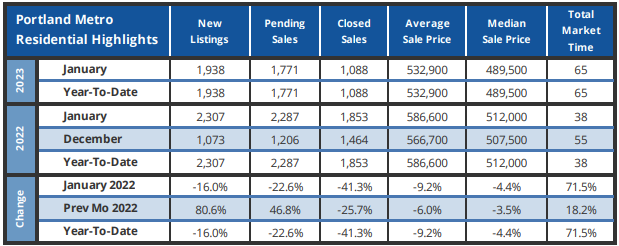

Portland Metro Area Real Estate Inventory/Price/Days on Market Report Through January 2023

Here’s an overview of the Portland, Oregon residential real estate market as of the end of January, 2023. Please keep in mind that Real Estate is Local. These numbers reflect the activity in the Portland Metro Area. If you’d like more specific information about your property or a specific neighborhood, Let’s Talk. Please reach out to me at 503-720-9393 or JonCohen@Windermere.com.

Inventory: The Sellers’ market continues as the inventory of homes sits at 2.7 months at the end of January and exceeding 2-months of supply for the 5th month in a row. For comparison, a balanced market is 4-6 months of inventory. Last year at this time, inventory was 0.8 months. Going back to January, 2020, pre-pandemic, inventory was 2.2 months, another sign we are moving back toward a more normal market.

Average and Median Home Price: While demand remains high, the supply of homes still is not sufficient to satisfy all buyers. We saw a decrease in the average price of homes in the entire metro area from $586,000 to $532,900 – a 9.2% drop from this time last year. However, the median price of metro area homes is now $489,500, down from $512,000 at this time last year decrease of 4.4%. This may be an indication that more lower-priced homes came on the market toward the end of 2022 as investors no longer wanted to be landlords, or simply wanted to cash out of their properties while prices were still high.

Days on Market: Although demand for homes remains high, higher mortgage interest rates and a more typical slowdown toward the end of 2022 have pushed the average number of days homes are on the active market to 65 days, up from 38 days in January 2022. Comparatively, the average days on market in January 2020 (pre-pandemic) was 74 days.

(Data and graphs provided by RMLS)

Bubble? What Bubble?

Two Reasons Why Today’s Housing Market Isn’t a Bubble

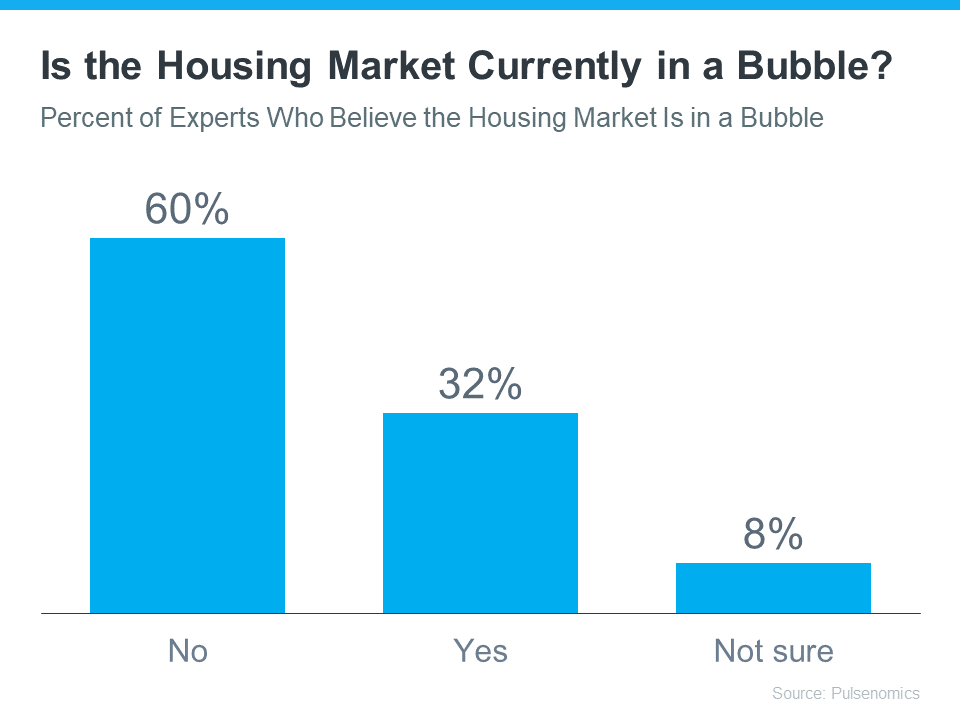

You may be reading headlines and hearing talk about a potential housing bubble or a crash, but it’s important to understand that the data and expert opinions tell a different story. A recent survey from Pulsenomics asked over one hundred housing market experts and real estate economists if they believe the housing market is in a bubble. The results indicate most experts don’t think that’s the case (see graph below):

As the graph shows, a strong majority (60%) said the real estate market is not currently in a bubble. In the same survey, experts give the following reasons why this isn’t like 2008:

As the graph shows, a strong majority (60%) said the real estate market is not currently in a bubble. In the same survey, experts give the following reasons why this isn’t like 2008:

- The recent growth in home prices is because of demographics and low inventory

- Credit risks are low because underwriting and lending standards are sound

If you’re concerned a crash may be coming, here’s a deep dive into those two key factors that should help ease your concerns.

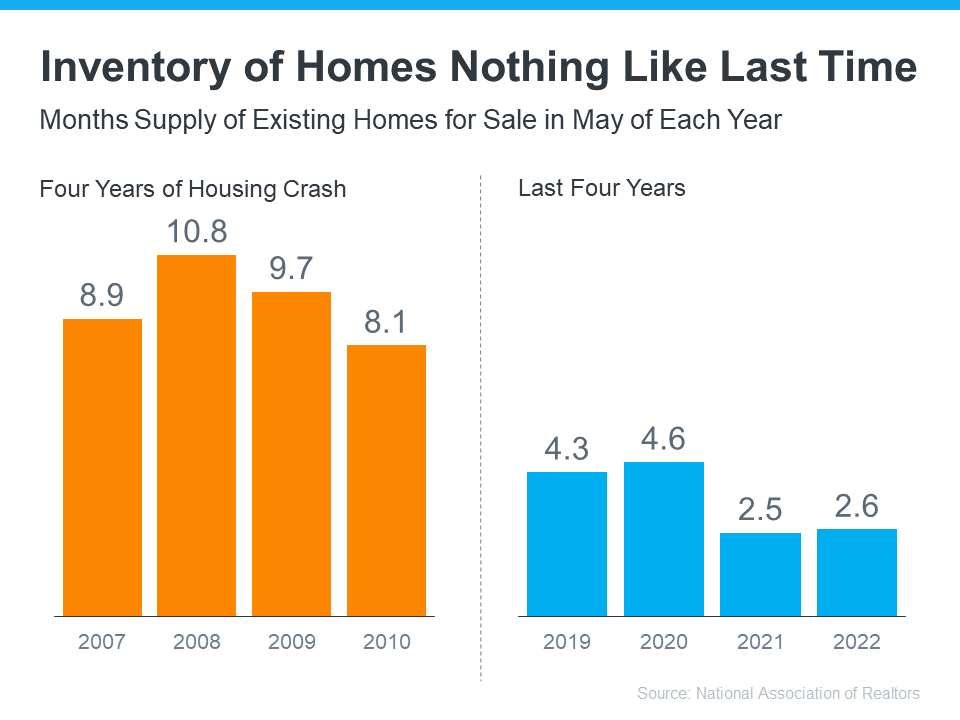

1. Low Housing Inventory Is Causing Home Prices To Rise

The supply of homes available for sale needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued price appreciation.

As the graph below shows, there were too many homes for sale from 2007 to 2010 (many of which were short sales and foreclosures), and that caused prices to tumble. Today, there’s still a shortage of inventory, which is causing ongoing home price appreciation (see graph below):

Inventory is nothing like the last time. Prices are rising because there’s a healthy demand for homeownership at the same time there’s a limited supply of homes for sale. Odeta Kushi, Deputy Chief Economist at First American, explains:

Inventory is nothing like the last time. Prices are rising because there’s a healthy demand for homeownership at the same time there’s a limited supply of homes for sale. Odeta Kushi, Deputy Chief Economist at First American, explains:

“The fundamentals driving house price growth in the U.S. remain intact. . . . The demand for homes continues to exceed the supply of homes for sale, which is keeping house price growth high.”

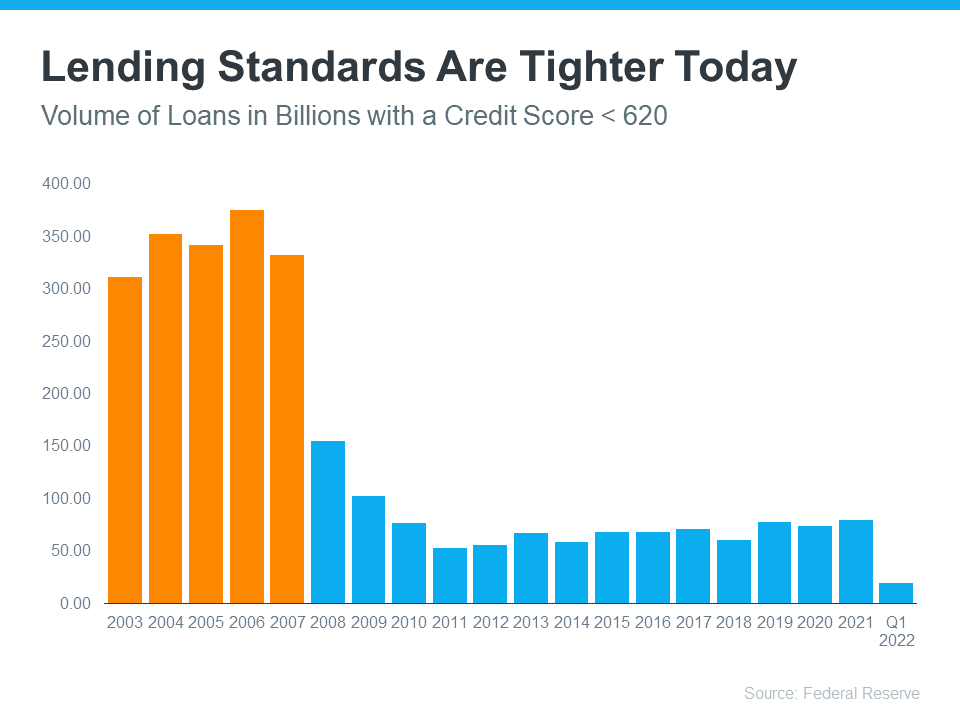

2. Mortgage Lending Standards Today Are Nothing Like the Last Time

During the housing bubble, it was much easier to get a mortgage than it is today. Here’s a graph showing the mortgage volume issued to purchasers with a credit score less than 620 during the housing boom, and the subsequent volume in the years after:

This graph helps show one element of why mortgage standards are nothing like they were the last time. Purchasers who acquired a mortgage over the last decade are much more qualified than they were in the years leading up to the crash. Realtor.com notes:

This graph helps show one element of why mortgage standards are nothing like they were the last time. Purchasers who acquired a mortgage over the last decade are much more qualified than they were in the years leading up to the crash. Realtor.com notes:

“. . . Lenders are giving mortgages only to the most qualified borrowers. These buyers are less likely to wind up in foreclosure.”

Bottom Line

A majority of experts agree we’re not in a housing bubble. That’s because home price growth is backed by strong housing market fundamentals and lending standards are much tighter today. If you have questions, let’s connect to discuss why today’s housing market is nothing like 2008.